US · Fed Press Conference

Tradl AI Read the brief →

tradl·decode Ep. 065

Geopolitical exhale, FOMC wall ahead

4:29 · two-voice

Shreya · Nilesh

Ed. 065 · Pre-market intelligenceTue · 16 Jun 2026 · 08:30 IST

Iran relief sparks risk-on surge

as FOMC dot-plot looms Wednesday.

▾ Today's Call Gap-up · FOMC overhang

- ↑Gift Nifty flags an ~80-point gap-up. Opening above 23,894 (central pivot) is needed to keep Monday's momentum from fading intraday.

- ●OI wall 23,750–24,000 defines the cage. Sustained trade above 24,000 opens the prior Gift Nifty high of 24,047 as the next reference.

- ↓Max-pain at 23,800 anchors the floor. A drift below 23,777 (Pivot S1) invalidates the Iran-relief bid and re-exposes the prior session low at 23,818.

- ↑Realty leads with a 3.96% Monday surge. Sector breadth — 15 of 17 sectors green — signals this was not a narrow beta trade but a broad risk-on rotation.

Support floor

23,750

Yesterday close

23,854

Resistance ceiling

24,000

S&P 500 +1.7% overnightVIX 14.24 · calm bandFII -1082 Cr T-1FOMC dot-plot Wed Jun 17Brent steady $83.48DII +5341 Cr T-1

01

Today's Trade Setups

★ Smart Chains · BetaPREDICT · 0 sessions left

Where does NIFTY close on 16 Jun expiry?

community pot

—

predictions cast

Defensive

When the band is wide and event risk is near, a defensive stance favours patience over exposure.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Balanced

A balanced read leans on the midpoint holding while the yield overhang stays unresolved.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Aggressive

An aggressive read positions for the band break that the overnight minutes could trigger.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Educational only · not advice. Smart Chains is an upcoming Tradl AI feature: cast a directional view, get the matching option chain with max profit / max loss / breakevens / R:R.

02

Previous Session

NIFTY 50

23,853.9▲ 231 · +0.98%

Last 7 sessions −0.21%−1.04%+0.52%−0.12%−0.23%+1.99%+0.98% Charts powered by TradingView

levels

Sensex

76,264.33

▲ 736.38 · +0.97%

Mirror of Nifty, same fade arc

levels

Bank Nifty

57,198.8

▲ 384 · +0.68%

Three-up streak, but weakest close

levels

Gift Nifty

23,934

▲ 80.1 · +0.34%

Overnight premium trails cash fade

03

Sector Lens

live

Where money is rotating. Every NSE sector vs Nifty — leading, lagging or turning — with a 250-session replay and a sector→stock drill-down.

Explore sector rotation → 04

Stocks in Focus

₹108−3.65%

Sentiment vacuum post-Sony merger collapse; no re-rating catalyst, sellers in control at 14d-low vicinity

Trigger · Close below 108 extends pressure toward the 83 14d-low band

₹7,344+2.58%

Defence and space order pipeline re-rated on geopolitical risk-premium expansion, +2.58% vs flat sector

Trigger · Above 7,344 prior close, sustained bid opens the path toward 14d-high territory above

₹581+4.65%

Ex-dividend stripping reverses post-record-date; underlying insurer demand stays intact on rate-cut arc

Trigger · Holding above 581 ex-div adjusted open keeps the 620 14d-high thesis alive

₹286+4.06%

LNG re-contracting optimism amplified by Iran-deal supply normalisation reducing spot-price risk

Trigger · Close above 286 toward 291 14d-high; failure back below 275 prior invalidates the breakout

₹4,880+3.62%

Crude steady near $83 Brent caps fuel-cost downside; Iran-deal relief rally boosts travel demand narrative

Trigger · Above 4,880 close, 4,942 14d-high is the next reference; below 4,710 prior negates the leg

₹158+3.44%

CV cycle re-rating on infrastructure spend momentum; risk-on tape lifts the entire commercial-vehicle complex

Trigger · Above 158, prior resistance band; a close here opens the 14d-high zone above 160

05

Pattern Sniper

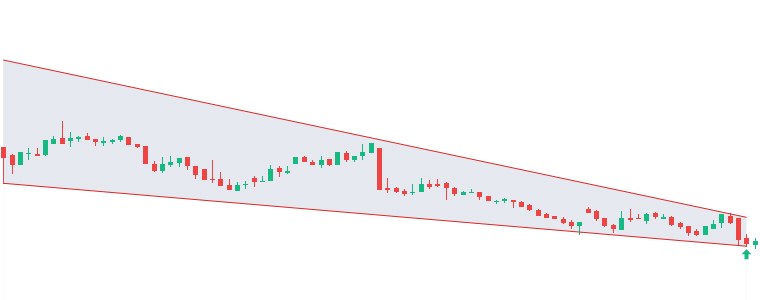

Falling Wedge ▲ BULL

AI 95%

The Falling Wedge is textbook with clean pivot points and a decisive breakout above the resistance line followed by a strong bullish move.

92%

Start 8 JunDetected 11 Jun 14:30

Inv. Head & Shoulders ▲ BULL

AI 90%

The geometry shows a clear inverse head and shoulders with well-defined pivots, followed by a sustained breakout and successful continuation above the neckline.

89%

Start 8 JunDetected 12 Jun 12:45

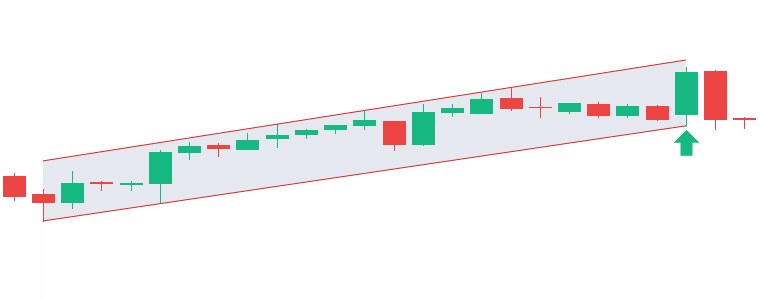

Ascending Channel ▲ BULL

AI 90%

The ascending channel shows well-defined parallel rails with multiple validation points for both support and resistance, confirming a strong bullish structure.

87%

Start 29 MayDetected 8 Jun 08:30

Falling Wedge ▲ BULL

AI 90%

The falling wedge is textbook, with both trendlines clearly defining a narrowing range and consistent pivot touches confirming the structure.

90%

Start 8 JunDetected 11 Jun 15:00

Inv. Head & Shoulders ▲ BULL

AI 90%

The inverse head and shoulders pattern is well-formed with clear pivot symmetry, and price has decisively broken the neckline and sustained the bullish…

91%

Start 9 JunDetected 12 Jun 12:15

Ascending Channel ▲ BULL

AI 90%

The ascending channel geometry is clean, with multiple valid pivot touches on both parallel trendlines and strong containment throughout the formation.

80%

Start 12 JunDetected 12 Jun 11:55

Pattern Detection Engine

6 patterns caught last session.

AI-verified chart formations across NSE-500 · timeframes 5m → 1h · match score > 80%.

— of 500 beta seats taken

06

Overnight Wire

Global Equities

S&P 5007,554

▲ 1.7%Broad risk appetite returns

Dow Jones51,671

▲ 0.9%Industrials lag tech surge

Nasdaq26,684

▲ 3.1%Tech leads Wall St rally

Nikkei 22569,246

▼ 0.2%Yen drag caps gains

KOSPI8,607

▲ 0.9%Korea tracks US momentum

Hang Seng24,737

▼ 0.4%Hong Kong retreats on caution

Commodities

Brent Crude$83.48

▲ 0.2%Supply calm holds floor

WTI Crude$81.13

▲ 0.73%Demand read nudges WTI

Comex Gold$4,337.90

▼ 0.2%Safe-haven bid fades

Rates · FX · Vol

Dollar Index99.7

▲ 0.16%Dollar steadies off lows

USD/INR94.70

◆ 0.00%Rupee holds range

US 30Y4.97%

◆ 0 bpsLong end holds steady

US 10Y4.47%

▼ 2 bpsFront end eases slightly

India 10Y6.87%

◆ 0 bpsIndia yield anchored

India VIX14.24

▼ 3.22%Fear premium compressing

Crypto· as of 07:30 IST

Bitcoin$66,367

▲ 1.06%Risk-on lifts Bitcoin

Ethereum$1,796.01

▲ 4.35%Ethereum outpaces crypto peers

07

Key Developments

Alert Caution Positive for India Neutral

GEOGeo

GEO06:36 IST

Oil prices steady as traders wait for more details on Strait of Hormuz reopening

GEOGeo

GEOGeo

GEO05:28 IST

Sensex, Nifty rally 1% as US-Iran peace hopes spark risk-on sentiment

GEOGeo

GEO05:05 IST

Dow Jones surges 500 points to record high, Nasdaq sees best day in three months on Iran deal

RBIPolicy

RBIPolicy

RBIPolicy

SEBIRegulator

SEBI00:00 IST

Settlement Order in the matter of Angel One Limited (Adjudication and Enquiry Proceedings)

08

Upcoming Catalysts

Expected market impact High Med Low

9:00 AMWed

17 JunWed

CYIENT · buyback record date

17 JunWed

BRIGADE · ex-bonus

Bonus 1:3 NSE

11:30 PMWed

18 JunThu

SBIN · board meeting

Fund Raising NSE

19 JunFri

HDFCBANK · ex-dividend

Dividend - Rs 13 Per Share NSE

19 JunFri

HDFCLIFE · ex-dividend

Dividend - Rs 2.10 Per Share NSE

5:00 PMFri

Monetary Policy Meeting Minutes

Don't miss a catalyst. Downloads a standard .ics file — import once into Google Calendar, Apple Calendar, or Outlook.

09

F&O Pulse

Nifty PCRneutral

0.96

PCR 0.96 · below 1.0 — neutral bias.

Max Pain16 Jun

23,800

Sits within range. 55 pts below close — magnet pull on quiet sessions.

F&O Heatlong/short OI

BANDHANBNK · GMRAIRPORT

Long: BANDHANBNK, GMRAIRPORT. Short: ONGC, HINDALCO.

Smart $ flowFII F&O

+4,180 Cr

FII building index-futures longs — risk-on positioning.

⊕ hover for FII option positioning

FII index-option positioning · net OI (contracts)

Index Calls

−2,09,020net

Long6.23L

Short8.32L

Δ day+84,905

Index Puts

+5,42,612net

Long11.94L

Short6.51L

Δ day+4,773

Options Battlefield · Nifty 16 Jun

Put writers (support) Call writers (resistance) Max Pain

23,750

0.39 Cr

23,800

Support

23,850

0.44 Cr

23,900

1.12 Cr

23,950

0.88 Cr

24,000

Resistance

2.22 Cr

MAX PAIN23,800 · 0.80 Cr

23,75023,80023,850 ●23,90023,95024,000

Put writers stacked at 23,800 PE (0.80 Cr OI) — that's the floor. Call writers stacked at 24,000 CE (2.22 Cr) — ceiling. The 23,800 max-pain magnet sits 55 pts below close: in a quiet session, that's where the market wants to gravitate. Decisive close outside 23,750–24,000 forces writer unwinding — a directional move follows.

10

Flows & VIX

Net cushion · DII absorbed FII outflows for a 13th straight session, net positive 4,259 Cr.

All figures · Cr · 15 Jun (T-1) provisional

FII CashT-1

−1,082

13th straight selling session.

13-day streak · −70,987 Cr cumulative

⊕ hover for FII F&O positioning

Index Futures+4,180 Cr

Index Calls−2,09,020 net

Index Puts+5,42,612 net

FII building index-futures longs — risk-on positioning.

NET

+4,259

DII pulling · floor holds

DII CashT-1

+5,341

Net cushion +4,259 Cr. DII absorbed the FII flow.

13-day absorption · 113% of FII

Calm < 15 band · ▼ 3.2% d/d

India VIX at 14.24, down 3.22% — Calm band reading favours premium sellers over hedgers near term.

Calm (<15) Moderate Elevated (20–25) Fear (>25)

11

Decode vs Reality

30-day rolling hit rateavg 60.4%

← 30 sessions agoyesterday →

Today's calls · live

Edition 065 · 16 Jun 2026 · grading EOD

Nifty holds the 23,650–24,100 band (±~1%) into the close.

LIVE

Nifty stays rangebound, 23,675–24,050 (±~0.8%) — our neutral call.

LIVE

Bank Nifty closes in the 56,650–57,750 band (±~1%).

LIVE

Realty stays in the top half of sectors today.

LIVE

Pharma stays in the bottom half today.

LIVE

Grading at 3:30 IST EOD · results tomorrow morning

Yesterday's calls · graded

Edition 064 · 15 Jun 2026 · EOD-graded

✗

Nifty holds the 23,400–23,850 band (±~1%) into the close.

Closed 23,854, above the 23,400–23,850 band.

✗

Nifty stays rangebound, 23,425–23,800 (±~0.8%) — our neutral call.

Closed 23,854, above the 23,425–23,800 band.

✓

Bank Nifty closes in the 56,250–57,400 band (±~1%).

Closed 57,199, inside the 56,250–57,400 band.

✓

Realty stays in the top half of sectors today.

Realty closed #1 of 22 (top_half).

✗

IT stays in the bottom half today.

IT closed #11 of 22, outside bottom_half.

12

The bigger picture

Geopolitical exhale meets Fed projection wall.

The Iran-deal relief rally handed Indian equities a broad 1% lift on Monday, with Dow Jones posting a 500-point record and Nasdaq logging its best session in three months. The move was genuine breadth, not a narrow bounce — 15 of 17 Nifty sectors closed green, with cyclicals like Realty, Consumer Durables, and Auto absorbing the bulk of the re-rating. VIX shedding 3.22% to 14.24 confirms the fear premium is deflating, not merely suppressed.

The counterforce arrives Wednesday Jun 17, when FOMC economic projections and the Fed dot-plot print at 23:30 IST — the prior longer-run rate projection sat at 3.1%. Until those dots are visible, FII caution persists: Monday's FII outflow of 1,082 Cr against DII absorption of 5,341 Cr shows domestic money defending while foreign capital waits for rate-path clarity. The US 30-year yield holding at 4.97% keeps the global cost-of-capital ceiling intact.

Within today's session, the sector rotation tells the cleaner story. Pharma and Healthcare are the lone laggards, suggesting the defensives are being unwound in favour of rate-sensitive and capex-linked plays — Realty, Infra, and Financials — which is consistent with a market pricing in rate relief ahead. That rotation persists only if Wednesday's dot-plot does not reprice the Fed's terminal rate upward.

Edition 065

Sources cross-verified before publish

NSEGovernment statisticsBSERBISEBICredit rating agenciesTrading EconomicsGlobal macro wireIndian financial pressTradl Pattern EngineTradl data platform

Every quantitative claim is cross-verified against at least two independent sources. Macro and policy claims sourced from primary regulators. AI-assisted synthesis with Tradl editorial review before publish.