CYIENT · buyback record date

Tradl AI Read the brief →

tradl·decode Ep. 066

Crude caves, dot-plot decides

3:49 · two-voice

Shreya · Nilesh

Ed. 066 · Pre-market intelligenceWed · 17 Jun 2026 · 08:30 IST

FOMC night, crude cave:

the dot-plot decides.

▾ Today's Call Fed-watch · crude tailwind

- ●OI wall band 23,850–24,100. Sustained trade above 24,032 (Pivot R1) would pressure the upper wall; failure to hold 23,960 central pivot re-opens the S1 at 23,917.

- ↑Brent collapses 4.6% to $79. Energy and Oil & Gas already repriced +1% Tuesday; downstream sectors absorb the input-cost relief narrative today.

- ↑VIX compresses to 13.39. A 6.68% single-session drop places fear firmly in the calm band, lowering the hedging premium that had capped index upside through last week.

- ↓Fed dot-plot at 23:30 IST. Current-year projection previously at 3.4%; any upward revision tightens the rate-path and pressures overnight FII positioning into Thursday's open.

Support floor

23,900

Yesterday close

23,989

Resistance ceiling

24,050

FOMC 23:30 ISTBrent 3-month lowVIX calm bandDII net buyer ₹3,189 CrMetals lagging -1.55%

01

Today's Trade Setups

★ Smart Chains · BetaPREDICT · 4 sessions left

Where does NIFTY close on 23 Jun expiry?

community pot

—

predictions cast

Defensive

When the band is wide and event risk is near, a defensive stance favours patience over exposure.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Balanced

A balanced read leans on the midpoint holding while the yield overhang stays unresolved.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Aggressive

An aggressive read positions for the band break that the overnight minutes could trigger.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Educational only · not advice. Smart Chains is an upcoming Tradl AI feature: cast a directional view, get the matching option chain with max profit / max loss / breakevens / R:R.

02

Previous Session

NIFTY 50

23,989.15▲ 135.25 · +0.57%

Last 7 sessions −1.04%+0.52%−0.12%−0.23%+1.99%+0.98%+0.57% Charts powered by TradingView

levels

Sensex

76,808.48

▲ 544.15 · +0.71%

Stronger d/d, close near session top

levels

Bank Nifty

57,297.15

▲ 98.35 · +0.17%

Four-day streak, momentum lagging peers

levels

Gift Nifty

24,006.5

▲ 17.35 · +0.07%

Flat overnight signal, four-day streak intact

03

Sector Lens

live

Where money is rotating. Every NSE sector vs Nifty — leading, lagging or turning — with a 250-session replay and a sector→stock drill-down.

Explore sector rotation → 04

Stocks in Focus

₹7,698+4.83%

Defence order pipeline re-rating drives +4.83% against a flat sector, signalling stock-specific accumulation

Trigger · Above 8,145 (14d-high) opens the prior breakout zone abandoned in the recent correction

₹111+2.49%

Media consolidation narrative revived; +2.49% on elevated volume suggests positioning ahead of corporate clarity

Trigger · Above 117 (14d-high) opens the next resistance band; below 108 invalidates the recovery thesis

₹720+5.28%

Bonus ex-date mechanics compress adjusted price, triggering fresh demand as float expands

Trigger · Holding above 684 (prior close pre-bonus) confirms demand absorption; break below opens 637

₹1,159+3.55%

Large-cap IT re-rating on deal-flow optimism outpaces sector; +3.55% with USD/INR tailwind adding margin relief

Trigger · Above 1,257 (14d-high) extends the recovery leg; below 1,119 invalidates the breakout base

₹1,089−1.70%

Profit-taking after a strong prior run; -1.7% with no sector support amplifies the pullback

Trigger · Below 1,060 (14d-low proxy) extends the corrective leg; reclaim of 1,106 reasserts demand

₹1,139+2.97%

Real estate demand spillover lifts building materials; tiles segment benefits from housing cycle momentum

Trigger · Above 1,143 (14d-high) clears the range ceiling and opens the next price discovery band

05

Pattern Sniper

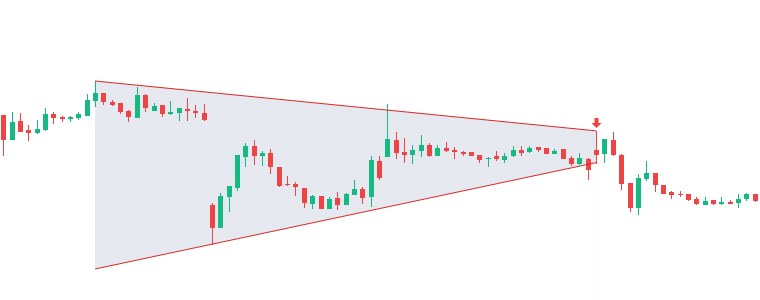

Symmetrical Triangle ▼ BEAR

AI 90%

The triangle features clear convergent trendlines with valid pivots, and price has decisively broken bearish, confirming the intended directional setup.

86%

Start 10 JunDetected 15 Jun 09:15

Double Bottom ▲ BULL

AI 90%

The double bottom structure is clean with well-defined pivots and clear breakout confirmation; price has decisively moved toward the target since the pattern…

87%

Start 16 JunDetected 16 Jun 12:40

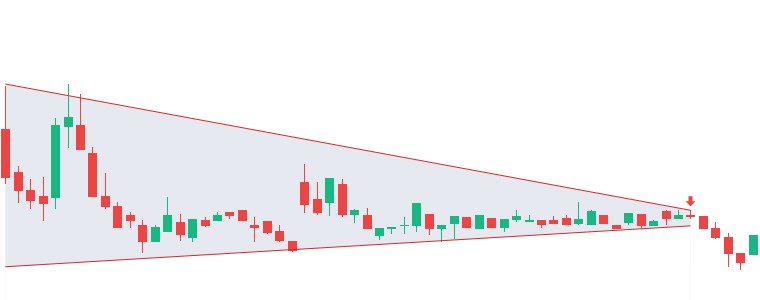

Falling Wedge ▲ BULL

AI 90%

The falling wedge is well-constructed with clear pivots confirming converging resistance and support lines; price has broken out above the upper boundary with…

90%

Start 5 JunDetected 12 Jun 09:30

Falling Wedge ▲ BULL

AI 90%

The falling wedge shows clean convergence with multiple confirmed touchpoints on both trendlines, accurately capturing the price compression within the…

82%

Start 8 JunDetected 11 Jun 14:15

Symmetrical Triangle ▼ BEAR

AI 90%

The symmetrical triangle shows clean pivot points on both converging trendlines, with a decisive downward breakout that has since followed through, confirming…

81%

Start 15 JunDetected 15 Jun 13:50

Ascending Channel ▲ BULL

AI 85%

The ascending channel shows clean pivot alignment on both rails with consistent parallel slope, confirming a valid short-term bullish consolidation structure.

82%

Start 15 JunDetected 16 Jun 10:50

Pattern Detection Engine

6 patterns caught last session.

AI-verified chart formations across NSE-500 · timeframes 5m → 1h · match score > 80%.

— of 500 beta seats taken

06

Overnight Wire

Global Equities

S&P 5007,511

▼ 0.6%Tech drag pulls benchmark

Dow Jones52,000

▲ 0.6%Value rotation lifts Dow

Nasdaq26,376

▼ 1.2%Growth selloff leads decline

Nikkei 22569,870

▲ 0.7%Yen relief lifts equities

KOSPI8,705

▲ 0.3%Modest Asia risk-on bid

Hang Seng24,527

▲ 0.1%Hong Kong stalls near flat

Commodities

Brent Crude$79.10

▼ 4.6%Demand fear pressures Brent

WTI Crude$75.54

▼ 6.38%Supply glut fear accelerates

Comex Gold$4,361.40

▲ 0.2%Dollar dip supports gold

Rates · FX · Vol

Dollar Index99.5

▼ 0.18%Dollar slips amid caution

USD/INR94.61

▼ 0.10%Rupee firms on inflows

US 30Y4.93%

▼ 4 bpsLong end eases modestly

US 10Y4.43%

▼ 4 bpsYields retreat four basis points

India 10Y6.87%

◆ 0 bpsIndia yields await catalyst

India VIX13.39

▼ 6.68%Fear premium compresses sharply

Crypto· as of 07:30 IST

Bitcoin$65,866

▼ 0.77%Bitcoin retreats below resistance

Ethereum$1,796.50

▲ 0.08%Ethereum holds near flat

07

Key Developments

Alert Caution Positive for India Neutral

GEOGeo

GEO06:58 IST

Oil prices slip below $80 for the first time in months ahead of Iran–U.S. peace deal on June 19

GEOGeo

GEOGeo

GEO06:17 IST

Aluminium stocks slide as US-Iran deal eases supply fears, ends war-driven rally

GEOGeo

RBIPolicy

RBIPolicy

SEBIRegulator

SEBI00:00 IST

Notice of Demand dated June 16, 2026 issued under RC No. 9161 of 2026 drawn against Rupee Services Private Limited in the matter of dealing in Illiquid Stocks Options at BSE

SEBIRegulator

08

Upcoming Catalysts

Expected market impact High Med Low

17 JunWed

17 JunWed

BRIGADE · ex-bonus

Bonus 1:3 NSE

11:30 PMToday

US · FOMC Economic Projections

18 JunThu

SBIN · board meeting

Fund Raising NSE

19 JunFri

HDFCBANK · ex-dividend

Dividend - Rs 13 Per Share NSE

19 JunFri

HDFCLIFE · ex-dividend

Dividend - Rs 2.10 Per Share NSE

5:00 PMFri

Monetary Policy Meeting Minutes

Don't miss a catalyst. Downloads a standard .ics file — import once into Google Calendar, Apple Calendar, or Outlook.

09

F&O Pulse

Nifty PCRbullish

1.03

PCR 1.03 · above 1.0 — bullish bias.

Max Pain23 Jun

23,900

Sits within range. 95 pts below close — magnet pull on quiet sessions.

F&O Heatlong/short OI

IDEA · CANBK

Long: IDEA, CANBK. Short: NTPC, ONGC.

Smart $ flowFII F&O

+429 Cr

FII index-futures positioning largely steady.

⊕ hover for FII option positioning

FII index-option positioning · net OI (contracts)

Index Calls

−2,52,327net

Long6.72L

Short9.25L

Δ day−43,307

Index Puts

+5,45,186net

Long11.45L

Short6.00L

Δ day+2,574

Options Battlefield · Nifty 23 Jun

Put writers (support) Call writers (resistance) Max Pain

23,850

0.07 Cr

23,900

23,950

0.16 Cr

24,000

S / R

0.76 Cr

24,050

0.08 Cr

24,100

0.24 Cr

MAX PAIN23,900 · 0.39 Cr

23,85023,90023,95024,000 ●24,05024,100

Put writers stacked at 24,000 PE (0.63 Cr OI) — that's the floor. Call writers stacked at 24,000 CE (0.76 Cr) — ceiling. The 23,900 max-pain magnet sits 95 pts below close: in a quiet session, that's where the market wants to gravitate. Decisive close outside 23,850–24,100 forces writer unwinding — a directional move follows.

10

Flows & VIX

Net cushion · DII absorbed the session heavily at ₹3,189 Cr; FII participation was marginal at ₹200 Cr.

All figures · Cr · 16 Jun (T-1) provisional

FII CashT-1

+200

1st straight buying session.

1-day streak · +200 Cr cumulative

⊕ hover for FII F&O positioning

Index Futures+429 Cr

Index Calls−2,52,327 net

Index Puts+5,45,186 net

FII index-futures positioning largely steady.

NET

+3,389

DII pulling · floor holds

DII CashT-1

+3,189

Net cushion +3,389 Cr. DII absorbed the FII flow.

1-day absorption · 1594% of FII

Calm < 15 band · ▼ 6.7% d/d

India VIX at 13.39, down 6.68% d/d, deep in calm territory — conditions favour premium sellers over hedgers.

Calm (<15) Moderate Elevated (20–25) Fear (>25)

11

Decode vs Reality

30-day rolling hit rateavg 64.8%

← 30 sessions agoyesterday →

Today's calls · live

Edition 066 · 17 Jun 2026 · grading EOD

Nifty holds the 23,750–24,200 band (±~1%) into the close.

LIVE

Nifty stays rangebound, 23,800–24,175 (±~0.8%) — our neutral call.

LIVE

Bank Nifty closes in the 56,700–57,850 band (±~1%).

LIVE

Realty stays in the top half of sectors today.

LIVE

Metals stays in the bottom half today.

LIVE

Grading at 3:30 IST EOD · results tomorrow morning

Yesterday's calls · graded

Edition 065 · 16 Jun 2026 · EOD-graded

✓

Nifty holds the 23,650–24,100 band (±~1%) into the close.

Closed 23,989, inside the 23,650–24,100 band.

✓

Nifty stays rangebound, 23,675–24,050 (±~0.8%) — our neutral call.

Closed 23,989, inside the 23,675–24,050 band.

✓

Bank Nifty closes in the 56,650–57,750 band (±~1%).

Closed 57,297, inside the 56,650–57,750 band.

✓

Realty stays in the top half of sectors today.

Realty closed #1 of 22 (top_half).

✓

Pharma stays in the bottom half today.

Pharma closed #15 of 22 (bottom_half).

12

The bigger picture

Disinflation pulse meets the Fed's next move.

The dominant force entering Wednesday is crude's capitulation. Brent's drop to $79 — a three-month low driven by an imminent Iran-US supply deal — rewires the inflation narrative faster than any central bank statement can. For India, cheaper crude compresses the current-account deficit, relieves fuel-subsidy pressure, and gives the RBI room it did not have even a fortnight ago. Everything today, though, routes through the FOMC Economic Projections at 23:30 IST, with the current-year dot previously anchored at 3.4%.

The floor has domestic scaffolding. DII cash inflows of 3,189 Cr on Tuesday — against FII's modest 200 Cr — signal that domestic institutions are not waiting for the Fed to deploy. India VIX at 13.39, its calmest read in weeks, means options markets are not pricing a shock; that removes one layer of mechanical selling pressure. Bank Nifty lagging at +0.17% versus Nifty's +0.57% is the counterweight — credit names need the dot-plot to cooperate before the 57,804 swing high becomes a credible target.

The rotation already visible — Realty leading at +2.26%, IT at +1.78%, Metals dragging at -1.55% — maps a rate-sensitive, domestically oriented playbook. Rate-sensitive sectors absorb the crude disinflation and a potential dovish dot revision; commodity-linked names face the opposite arithmetic. That divergence likely widens rather than closes until the 23:30 IST print resets the calculus.

Edition 066

Sources cross-verified before publish

NSEGovernment statisticsBSERBISEBICredit rating agenciesTrading EconomicsGlobal macro wireIndian financial pressTradl Pattern EngineTradl data platform

Every quantitative claim is cross-verified against at least two independent sources. Macro and policy claims sourced from primary regulators. AI-assisted synthesis with Tradl editorial review before publish.