US · Fed Waller Speech

Tradl AI Read the brief →

tradl·decode Ep. 069

Gap-up meets IT wreckage and Iran fog

4:15 · two-voice

Shreya · Nilesh

Ed. 069 · Pre-market intelligenceMon · 22 Jun 2026 · 08:30 IST

Gift Nifty gaps up 140 points as Wall Street surges,

but the IT wreckage and Iran fog complicate the open.

▾ Today's Call Gap-up clouded · IT overhang

- ↑Gift Nifty +0.58%, gap-up into resistance. Opening print near 24,152 runs straight into the OI wall band ceiling — supply hasn't cleared yet.

- ↓IT sector -3.65%, INFY leads the damage. INFY's -6.76% single-session move signals earnings-driven de-rating, not a sector rotation dip.

- ●OI wall band 23,900–24,150 caps the range. A sustained close above 24,150 opens the 5-day swing high at 24,206; below 23,928 invalidates the pivot support thesis.

- ↑Fed Waller speaks at 18:30 IST today. Tone hawkish or dovish relative to US 30Y at 4.90% will reprice rate-sensitive financials into Tuesday's open.

Support floor

23,900

Yesterday close

24,013

Resistance ceiling

24,100

IT rout: -3.65%Gift Nifty +140 ptsHormuz tension bidVIX calm at 12.97FII net buyer ₹4,859 CrWaller speech 18:30 IST

01

Today's Trade Setups

★ Smart Chains · BetaPREDICT · 1 sessions left

Where does NIFTY close on 23 Jun expiry?

community pot

—

predictions cast

Defensive

When the band is wide and event risk is near, a defensive stance favours patience over exposure.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Balanced

A balanced read leans on the midpoint holding while the yield overhang stays unresolved.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Aggressive

An aggressive read positions for the band break that the overnight minutes could trigger.

Max profit

₹—

Max loss

₹—

R:R · —Lots · 1

Educational only · not advice. Smart Chains is an upcoming Tradl AI feature: cast a directional view, get the matching option chain with max profit / max loss / breakevens / R:R.

02

Previous Session

NIFTY 50

24,013.1▼ 154.9 · −0.64%

Last 7 sessions −0.23%+1.99%+0.98%+0.57%+0.40%+0.34%−0.64% Charts powered by TradingView

levels

Sensex

76,802.9

▼ 607.08 · −0.78%

Deepest drop, mirrored Nifty recovery

levels

Bank Nifty

57,685.75

▼ 278.05 · −0.48%

Narrowest range, early high faded

levels

Gift Nifty

24,152

▲ 138.9 · +0.58%

Overnight futures signal gap-up open

03

Sector Lens

live

Where money is rotating. Every NSE sector vs Nifty — leading, lagging or turning — with a 250-session replay and a sector→stock drill-down.

Explore sector rotation → 04

Stocks in Focus

₹1,409+7.51%

Defence order momentum driving re-rating; 14d-range breakout compresses short float

Trigger · Above 1,443 (14d-high) extends the re-rating leg; below 1,310 invalidates the breakout thesis

₹1,051−6.76%

Guidance cut or earnings miss triggered institutional de-grossing; gap-down from 1,128 prior

Trigger · Close below 1,030 (14d-low) opens a leg toward multi-month support; above 1,128 needed to repair

₹8,374+0.83%

Defence and space capex tailwind sustaining incremental demand for precision components

Trigger · Holding above prior session close; a breach of 14d-low would signal fading momentum

₹780−2.63%

Rising India 10Y at 6.85% compresses NIM expectations; sector rotation out of large private banks

Trigger · Below 737 (14d-low) opens the next support band; above 803 (14d-high) resets the bear thesis

₹725+2.01%

Tourism demand resilience and sector rotation into domestic consumption names driving the bid

Trigger · Above 729 (14d-high) extends the recovery; below 710 prior session close softens near-term momentum

₹1,423+1.86%

Pipeline infra order flow keeps steel tube demand elevated; metals sector bid supporting

Trigger · Above 1,434 (14d-high) opens fresh ground; below 1,397 prior session close fades the bull case

05

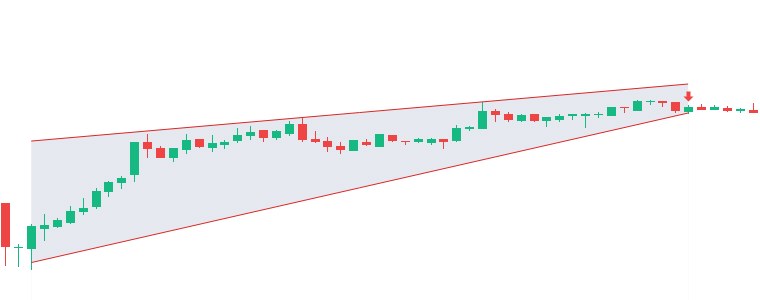

Pattern Sniper

Symmetrical Triangle ▲ BULL

AI 90%

The symmetrical triangle exhibits clear, converging trendlines with multiple distinct touch points on both sides and a strong, impulsive breakout candle that…

85%

Start 16 JunDetected 18 Jun 14:00

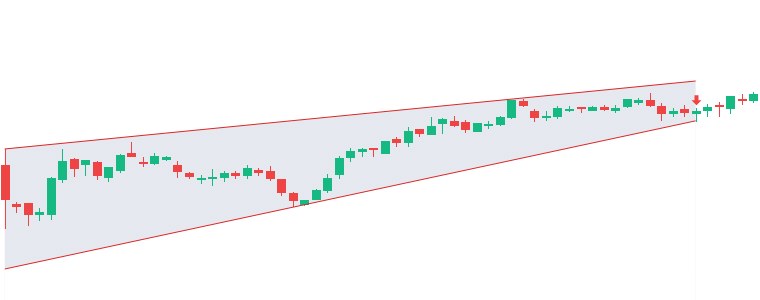

Rising Wedge ▼ BEAR

AI 95%

The rising wedge is geometrically precise with clean pivot touches on both lines, and price has decisively broken the lower support line with follow-through.

88%

Start 18 JunDetected 18 Jun 13:40

Falling Wedge ▲ BULL

AI 90%

The falling wedge is well-defined with clear, respecting pivots on both the upper resistance and lower support lines, showing good convergence.

83%

Start 13 MayDetected 15 Jun 09:30

Falling Wedge ▲ BULL

AI 90%

The falling wedge shows clean convergence with multiple valid touch points, followed by a decisive bullish breakout that has successfully resolved toward the…

89%

Start 12 JunDetected 18 Jun 09:30

Ascending Triangle ▲ BULL

AI 90%

The ascending triangle shows clean, rising support pivots and a firm horizontal resistance breakout, with price successfully continuing momentum after piercing…

80%

Start 18 JunDetected 18 Jun 13:50

Rising Wedge ▼ BEAR

AI 85%

The rising wedge exhibits well-defined converging trendlines with multiple pivot touches on both sides, confirming a valid contraction phase.

81%

Start 18 JunDetected 18 Jun 14:15

Pattern Detection Engine

6 patterns caught last session.

AI-verified chart formations across NSE-500 · timeframes 5m → 1h · match score > 80%.

— of 500 beta seats taken

06

Overnight Wire

Global Equities

S&P 5007,501

▲ 1.1%Tech-led broad advance

Dow Jones51,565

▲ 0.1%Blue-chips lag tech surge

Nasdaq26,518

▲ 1.9%Growth names drive rally

Nikkei 22572,376

▲ 2.0%Risk appetite lifts Japan

KOSPI9,212

▲ 1.7%Korea joins risk-on bid

Hang Seng23,528

▼ 1.7%Hong Kong diverges lower

Commodities

Brent Crude$79.34

▲ 0.2%Supply calm, marginal bid

WTI Crude$75.56

▲ 0.40%Demand narrative holds

Comex Gold$4,218.60

▲ 1.2%Safe-haven demand firms

Rates · FX · Vol

Dollar Index100.8

▼ 0.13%Dollar softness lingers

USD/INR94.31

▼ 0.01%Rupee near-flat, range-bound

US 30Y4.90%

▼ 2 bpsLong end pressure eases

US 10Y4.45%

▼ 1 bpsYield drift, mild relief

India 10Y6.85%

▲ 1 bpsDomestic yields edge up

India VIX12.97

▲ 2.34%Calm band, slight uptick

Crypto· as of 07:30 IST

Bitcoin$64,583

▲ 0.47%Crypto consolidates gains

Ethereum$1,743.83

▲ 0.28%Ethereum awaits catalyst

07

Key Developments

Alert Caution Positive for India Neutral

GEOGeo

GEO07:21 IST

Oil edges higher on Strait of Hormuz tensions; Brent hovers near $80 per barrel amid volatility

GEOGeo

GEO07:01 IST

Asian Markets Today: Japan's Nikkei, South Korea's Kospi In Green, Hang Seng Down 2% Over US-Iran Deal Uncerta

GEOGeo

GEO06:54 IST

Nifty Outlook for June 22: 24,000 remains the key for index as US-Iran uncertainties remain

GEOGeo

GEO06:50 IST

Iran Pauses Peace Talks After Trump's 'Will Hit Hard' Warning Over Hezbollah; US Says Talks Continue

NSEMarkets

NSEMarkets

SEBIRegulator

SEBI14:18 IST

3i Infotech Ltd: Please find attached Intimation letter that Company has received an Order from a leading UAE-based tech

NSEMarkets

08

Upcoming Catalysts

Expected market impact High Med Low

6:30 PMToday

23 JunTue

HINDUNILVR · ex-dividend

Dividend - Rs 22 Per Share NSE

23 JunTue

ASIANPAINT · ex-dividend

Dividend - Rs 23 Per Share NSE

9:00 AMWed

US · Fed Bank Stress Test Results

24 JunWed

BAJAJ-AUTO · buyback record date

24 JunWed

ZFCVINDIA · ex-bonus

Bonus 5:1 NSE

9:00 AMThu

US · Fed Goolsbee Speech

9:00 AMThu

US · Fed Williams Speech

25 JunThu

INDUSINDBK · ex-dividend

Dividend - Rs 1.50 Per Share NSE

6:00 PMThu

Don't miss a catalyst. Downloads a standard .ics file — import once into Google Calendar, Apple Calendar, or Outlook.

09

F&O Pulse

Nifty PCRneutral

0.78

PCR 0.78 · below 1.0 — neutral bias.

Max Pain23 Jun

24,000

Sits within range. 13 pts below close — magnet pull on quiet sessions.

F&O Heatlong/short OI

IDFCFIRSTB · ADANIPOWER

Long: IDFCFIRSTB, ADANIPOWER. Short: WIPRO, SUZLON.

Smart $ flowFII F&O

−891 Cr

FII index futures stay net short — defensive positioning.

⊕ hover for FII option positioning

FII index-option positioning · net OI (contracts)

Index Calls

−3,00,320net

Long6.40L

Short9.40L

Δ day−59,641

Index Puts

+6,29,690net

Long11.58L

Short5.28L

Δ day+67,027

Options Battlefield · Nifty 23 Jun

Put writers (support) Call writers (resistance) Max Pain

23,900

0.67 Cr

23,950

0.48 Cr

24,000

S / R

24,050

0.50 Cr

24,100

0.81 Cr

24,150

0.42 Cr

MAX PAIN24,000 · 1.11 Cr

23,90023,95024,000 ●24,05024,10024,150

Put writers stacked at 24,000 PE (1.11 Cr OI) — that's the floor. Call writers stacked at 24,000 CE (1.06 Cr) and 24,100 CE (0.81 Cr) — ceiling. The 24,000 max-pain magnet sits 13 pts below close: in a quiet session, that's where the market wants to gravitate. Decisive close outside 23,900–24,150 forces writer unwinding — a directional move follows.

10

Flows & VIX

Net cushion · FII flipped to net buyers at ₹4,859 Cr, outpacing ₹1,160 Cr of DII selling — net inflow ₹3,699 Cr.

All figures · Cr · 21 Jun (T-1) provisional

FII CashT-1

+4,859

1st straight buying session.

1-day streak · +4,859 Cr cumulative

⊕ hover for FII F&O positioning

Index Futures−891 Cr

Index Calls−3,00,320 net

Index Puts+6,29,690 net

FII index futures stay net short — defensive positioning.

NET

+3,699

FII pulling · floor holds

DII CashT-1

−1,160

Net cushion +3,699 Cr. FII bid outweighed DII selling.

1-day streak

Calm < 15 band · ▲ 2.3% d/d

India VIX at 12.97 (+2.34% d/d) stays in the calm band, favouring defined-range strategies over directional momentum plays.

Calm (<15) Moderate Elevated (20–25) Fear (>25)

11

Decode vs Reality

30-day rolling hit rateavg 68.6%

← 30 sessions agoyesterday →

Today's calls · live

Edition 069 · 22 Jun 2026 · grading EOD

Nifty holds the 23,800–24,250 band (±~1%) into the close.

LIVE

Nifty stays rangebound, 23,825–24,200 (±~0.8%) — our neutral call.

LIVE

Bank Nifty closes in the 57,100–58,250 band (±~1%).

LIVE

Healthcare stays in the top half of sectors today.

LIVE

IT stays in the bottom half today.

LIVE

Grading at 3:30 IST EOD · results tomorrow morning

Yesterday's calls · graded

Edition 068 · 21 Jun 2026 · EOD-graded

✓

Nifty holds the 23,950–24,400 band (±~1%) into the close.

Closed 24,013, inside the 23,950–24,400 band.

✓

Nifty stays rangebound, 23,975–24,350 (±~0.8%) — our neutral call.

Closed 24,013, inside the 23,975–24,350 band.

✓

Bank Nifty closes in the 57,400–58,550 band (±~1%).

Closed 57,686, inside the 57,400–58,550 band.

✓

Healthcare stays in the top half of sectors today.

Healthcare closed #1 of 17 (top_half).

✓

IT stays in the bottom half today.

IT closed #17 of 17 (bottom_half).

12

The bigger picture

A split market: defensive rotation meets geopolitical crude risk.

The dominant force entering the week is a tug-of-war between offshore optimism and domestic sector damage. S&P 500's 1.1% Friday rally is gifting a gap-up open, but INFY's -6.76% drop has cracked IT's structural premium, and the sector rarely bounces cleanly in the session immediately after an earnings-driven de-rating of that magnitude. Healthcare, Pharma, and Defence leading Friday's tape tells you where domestic money was already rotating before this gap.

The bid argument flips to foreign money: FII turned net buyers at ₹4,859 Cr, outpacing ₹1,160 Cr of DII selling to hold the index above 24,000. Max pain at 24,000 and India VIX pinned at 12.97 — a multi-month calm band — suggest option writers are not pricing a breakdown, which limits the downside unless Hormuz risk escalates into a supply disruption, not just a tension premium. Brent at $79.34 is a tax on Oil & Gas earnings, not yet a macro shock.

The rotation trade this week favours defensives over rate-sensitives. Healthcare, Pharma, and Defence absorbed Friday's selling pressure, and with Fed Waller speaking today at 18:30 IST and Bank Stress Test results due Wed Jun 24, financials and private banks face event risk on both sides before the week resolves. IT's weight in the index means the gap-up may fade unless fresh sector leadership fills the void.

Edition 069

Sources cross-verified before publish

NSEGovernment statisticsBSERBISEBICredit rating agenciesTrading EconomicsGlobal macro wireIndian financial pressTradl Pattern EngineTradl data platform

Every quantitative claim is cross-verified against at least two independent sources. Macro and policy claims sourced from primary regulators. AI-assisted synthesis with Tradl editorial review before publish.